MEDDPICC Sales Methodology Guide for Financial Services

Master MEDDPICC qualification for financial services sales. Learn regulatory stakeholder mapping, risk-focused qualification, and conservative approval processes for banks, insurance, and investment firms.

Financial services sales involves risk-averse decision-makers, strict regulatory oversight, and conservative buying processes. Here's how to use MEDDPICC qualification framework specifically for banks, insurance companies, and investment firms - plus how to practice these sophisticated qualification conversations.

Selling to financial services is uniquely challenging. You're navigating regulatory compliance, risk management committees, fiduciary responsibilities, security requirements, and multi-stakeholder approval processes that can take 12-24 months. Traditional qualification frameworks often miss the financial services-specific complexity that determines deal success.

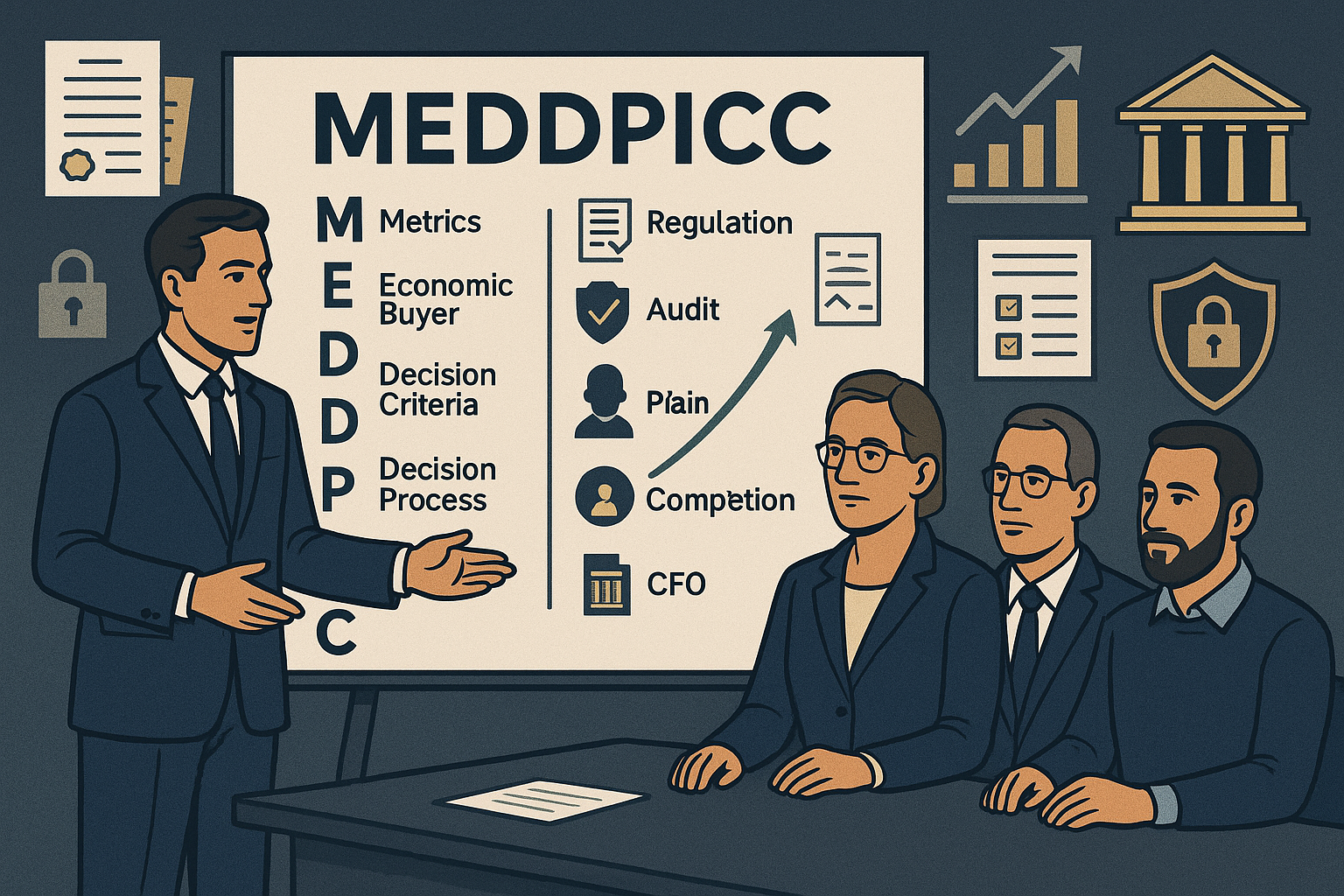

MEDDPICC (Metrics, Economic Buyer, Decision Criteria, Decision Process, Paper Process, Identify Pain, Champion, Competition) works powerfully for financial services because it forces disciplined qualification across all the dimensions that matter - from regulatory compliance to risk management to conservative approval processes.

But executing MEDDPICC in financial services requires understanding regulatory environments, risk management priorities, and conservative decision-making cultures. You need to practice qualifying deals with prospects who think in terms of regulatory risk, compliance obligations, and fiduciary responsibilities.

This guide shows you exactly how to apply MEDDPICC to financial services sales, including regulatory-specific qualification questions, risk stakeholder mapping, and how to practice until MEDDPICC becomes second nature in financial environments.

Why Financial Services Needs MEDDPICC

Financial Services Sales Complexity:

- Multiple regulatory stakeholders (compliance, risk, legal, audit)

- Strict regulatory oversight (OCC, FDIC, SEC, state regulators)

- Conservative, risk-averse decision-making culture

- Long sales cycles (12-24+ months typical)

- Complex integration with core banking/insurance systems

- Fiduciary responsibilities and customer protection obligations

Traditional Qualification Failures:

- Missing key compliance and risk stakeholders

- Underestimating regulatory approval requirements

- Not understanding conservative budget processes

- Failing to identify risk management champions

- Ignoring competitive incumbent relationships

- Missing paper process complexity (security audits, regulatory approvals)

MEDDPICC Framework for Financial Services

M - Metrics (Regulatory and Business Outcomes)

Purpose: Quantify the compliance, risk, and financial impact your solution must deliver.

Financial Services Metrics to Identify:

Regulatory Compliance Metrics:

- "What regulatory metrics are you measured against?"

- "What's your current examination rating?"

- "How many regulatory findings do you have annually?"

- "What compliance scores need improvement?"

Risk Management Metrics:

- "What operational risk incidents occur monthly?"

- "What's your fraud loss rate / detection rate?"

- "How many security incidents do you experience?"

- "What's your risk tolerance for [relevant area]?"

Financial Performance Metrics:

- "What's the cost of manual compliance processes?"

- "How much revenue is at risk from regulatory issues?"

- "What's your current efficiency ratio?"

- "What ROI do you require for technology investments?"

Customer Impact Metrics:

- "What's your customer complaint rate?"

- "How long does account opening / loan processing take?"

- "What's your customer satisfaction score?"

- "What's your customer retention rate?"

Example Financial Services Metrics:

- Reduce compliance processing time by 40%

- Decrease regulatory findings by 60%

- Improve fraud detection rate to 95%+

- Achieve examination rating upgrade

- Reduce operational risk incidents by 50%

E - Economic Buyer (Financial Services Budget Authority)

Purpose: Identify who has final budget authority for technology and compliance investments.

Financial Services Economic Buyers:

Typical Economic Buyers by Organization:

- Community Banks: CFO or President/CEO

- Regional Banks: CFO, CTO, or COO

- Insurance Companies: CFO or CIO

- Investment Firms: COO or CTO

- Credit Unions: CEO or CFO

Qualifying Questions:

- "Who ultimately approves technology investments over $[amount]?"

- "What's your annual budget for compliance technology?"

- "Who owns the budget for risk management solutions?"

- "How are IT and compliance budgets allocated?"

- "Who approved your last major technology purchase?"

Financial Services Budget Complexity:

- Multiple budget sources (IT, compliance, operations, risk)

- Capital vs. operating expense distinctions

- Regulatory examination-driven budget priorities

- Board approval requirements for large purchases

Red Flags:

- Can't identify specific economic buyer

- "Committee decides" without named budget owner

- Economic buyer not concerned about regulatory issues

- Budget source unclear or unfunded

- No urgency despite regulatory pressures

D - Decision Criteria (Regulatory and Technical Requirements)

Purpose: Understand the formal and informal criteria that will determine vendor selection.

Financial Services Decision Criteria:

Regulatory Compliance Criteria:

- "What regulatory requirements must be met?"

- "What compliance certifications do you require?"

- "What audit and reporting capabilities are essential?"

- "What regulatory documentation is mandatory?"

Risk Management Criteria:

- "What security and data protection standards must we meet?"

- "What operational risk controls are required?"

- "How do you evaluate vendor risk?"

- "What business continuity requirements do you have?"

Technical Criteria:

- "What core systems must we integrate with?"

- "What security standards are mandatory (SOC 2, ISO 27001)?"

- "What uptime and availability requirements do you have?"

- "What disaster recovery capabilities are required?"

Business Criteria:

- "What ROI timeline are you expecting?"

- "What vendor financial stability do you require?"

- "What implementation timeline is acceptable?"

- "What ongoing support requirements are essential?"

Weighted Criteria Exercise: Ask prospects to rank criteria importance:

- Regulatory compliance: High/Medium/Low

- Risk management: High/Medium/Low

- Integration capability: High/Medium/Low

- Cost/ROI: High/Medium/Low

- Vendor stability: High/Medium/Low

D - Decision Process (Financial Services Approval Workflow)

Purpose: Map the complete decision-making process from evaluation to contract signature.

Financial Services Decision Process Questions:

Process Mapping:

- "Walk me through how you've made similar technology decisions?"

- "Who needs to be involved at each stage?"

- "What committees need to review and approve?"

- "How long did your last major technology purchase take?"

Financial Services-Specific Stages:

- Initial evaluation (business case development)

- Risk assessment (vendor risk review, security evaluation)

- Compliance review (regulatory requirements validation)

- IT assessment (technical integration, security review)

- Financial analysis (CFO ROI approval)

- Committee approvals (technology committee, risk committee, board)

- Legal review (contract negotiation)

- Regulatory notification (if required)

- Final executive approval

Timeline Questions:

- "What's your target decision timeline?"

- "When is your next regulatory examination?"

- "Are there any compliance deadlines driving urgency?"

- "What could accelerate or delay this timeline?"

Red Flags:

- Vague or undefined process

- No clear timeline or milestones

- Key risk/compliance stakeholders not identified

- Process owner not designated

- No examination or regulatory pressure creating urgency

P - Paper Process (Financial Services Contract Complexity)

Purpose: Understand the contracting, legal, and regulatory documentation requirements.

Financial Services Paper Process:

Financial Services-Specific Documents:

- Vendor Risk Assessment - Third-party risk evaluation

- Security Audit Reports - SOC 2, penetration testing results

- Regulatory Compliance Documentation - How solution meets regulations

- Business Continuity Plans - Disaster recovery and redundancy

- Service Level Agreements - Uptime and performance guarantees

- Data Security Agreements - Data protection and privacy commitments

- Insurance Certificates - Cyber liability, E&O insurance

- Financial Stability Documentation - Vendor financial statements

Qualifying Questions:

- "What vendor risk assessment process do you follow?"

- "What security documentation and audits are required?"

- "Who reviews and approves vendor contracts?"

- "How long does your legal and compliance review typically take?"

- "What regulatory approvals or notifications are needed?"

Financial Services Procurement Complexity:

- Vendor risk management committee review

- Information security officer approval

- Compliance officer sign-off

- Legal department contract review

- Board approval for large purchases

- Regulatory notification requirements

Timeline Impact:

- Vendor risk assessment: 4-8 weeks

- Security audit review: 2-4 weeks

- Legal review: 6-12 weeks

- Committee approvals: 4-8 weeks each

- Regulatory notification: 30-90 days (if required)

Red Flags:

- No understanding of paper process requirements

- Underestimating timeline for risk assessment

- Missing critical compliance documents

- Legal/compliance/risk not engaged

- No vendor risk process defined

I - Identify Pain (Regulatory and Operational Problems)

Purpose: Uncover compelling compliance, risk, and operational problems that drive urgency.

Financial Services Pain Identification:

Regulatory Compliance Pain:

- "What regulatory concerns keep you up at night?"

- "What examination findings have you received?"

- "Where are you most vulnerable in regulatory audits?"

- "What compliance gaps need to be addressed?"

Risk Management Pain:

- "What operational risks are you most concerned about?"

- "Where have you experienced security incidents or fraud?"

- "What third-party risks worry you most?"

- "How confident are you in your current risk monitoring?"

Operational Efficiency Pain:

- "What manual processes consume too much staff time?"

- "Where are you seeing operational errors or inefficiencies?"

- "What processes slow down customer service?"

- "How does current technology limit business growth?"

Competitive and Business Pain:

- "How do technology limitations affect competitiveness?"

- "Where are you losing customers to competitors?"

- "What business opportunities can't you pursue due to constraints?"

- "How do legacy systems hold back innovation?"

Pain Quantification:

- Cost of regulatory findings: $ in remediation

- Risk of non-compliance: $ in potential fines

- Staff time wasted: hours per week

- Revenue at risk: $ per quarter

- Customer losses: $ annually

Red Flags:

- No clear, compelling pain

- Pain not urgent or regulatory-driven

- Economic buyer doesn't feel the pain

- No quantified impact or consequences

C - Champion (Compliance or Risk Advocate)

Purpose: Identify and develop internal advocates who will sell for you when you're not in the room.

Financial Services Champion Characteristics:

Ideal Champion Profile:

- Has political capital and respect in organization

- Personally responsible for area your solution improves

- Has access to economic buyer and risk/compliance leaders

- Willing to advocate internally for your solution

- Understands both regulatory and business value

Financial Services Champion Types:

- Compliance Champion: Chief Compliance Officer or Compliance Manager

- Risk Champion: Chief Risk Officer or Risk Manager

- Technology Champion: CIO/CTO who supports technical fit

- Operations Champion: COO focused on efficiency and risk reduction

- Executive Champion: CEO or board member with strategic vision

Champion Development Questions:

- "Who internally is most impacted by [regulatory/risk problem]?"

- "Who has successfully championed technology adoption before?"

- "Who has the ear of [economic buyer] on risk matters?"

- "Who would benefit most from solving this problem?"

Champion Enablement:

- Provide regulatory compliance evidence

- Share risk mitigation ROI calculations

- Offer reference calls with similar institutions

- Create executive summary for board presentation

- Coach on how to present to risk committees

Testing Champion Strength:

- Will they arrange meetings with risk/compliance stakeholders?

- Do they share internal examination findings and concerns?

- Will they present your solution in committee meetings?

- Do they coach you on organizational politics and priorities?

Red Flags:

- No clear champion identified

- Champion lacks organizational influence

- Champion not personally responsible for pain area

- Champion won't take action to advance deal

- Champion doesn't have economic buyer access

C - Competition (Alternative Solutions and Status Quo)

Purpose: Understand competitive alternatives and why prospects might choose them.

Financial Services Competition:

Competitive Landscape:

- Direct competitors: Other fintech/regtech vendors

- Incumbent solutions: Current systems and processes

- Status quo: Continue with manual or existing approach

- Build internally: IT/compliance team creates custom solution

Competition Qualifying Questions:

- "What other solutions are you evaluating?"

- "How long have you been with your current provider?"

- "What do you like about their approach?"

- "What concerns do you have about [competitor]?"

- "How satisfied are you with your current process?"

- "Have you considered building something internally?"

Financial Services Competitive Factors:

- Incumbent relationships: Long-standing vendor relationships and risk aversion

- Regulatory approval: Current solution already approved by regulators

- Integration established: Existing system integrations and workflows

- Change risk: Fear of operational disruption during transition

- Conservative culture: Preference for proven, established solutions

Competitive Strategy:

- Map your strengths to their regulatory criteria

- Identify competitor regulatory/security weaknesses

- Address status quo with examination timing urgency

- Differentiate on compliance outcomes and risk reduction

Red Flags:

- Unwilling to discuss competitors or alternatives

- Already committed to incumbent renewal

- Status quo has strong internal support

- No compelling regulatory event forcing change

- Risk-averse culture preventing consideration of alternatives

Financial Services MEDDPICC Qualification Checklist

Fully Qualified Deal Requirements:

✅ Metrics:

- Quantified regulatory compliance targets

- Measurable risk reduction goals

- Clear financial/ROI requirements

- Defined operational efficiency metrics

✅ Economic Buyer:

- Budget owner identified by name and title

- Budget amount and source confirmed

- Economic buyer concerned about regulatory/risk issues

- Authority level validated

✅ Decision Criteria:

- Regulatory requirements documented

- Risk management criteria defined

- Technical and security criteria clear

- Weighted importance established

✅ Decision Process:

- Process stages and committees mapped

- Timeline and regulatory milestones defined

- All stakeholders identified (compliance, risk, IT, legal)

- Process owner designated

✅ Paper Process:

- Vendor risk assessment requirements known

- Security audit and documentation process defined

- Legal review timeline estimated

- Regulatory notification needs understood

✅ Identify Pain:

- Compelling regulatory or risk pain articulated

- Pain quantified financially

- Examination timing or regulatory urgency established

- Economic buyer personally concerned

✅ Champion:

- Champion identified and engaged

- Champion has compliance/risk responsibility

- Champion has organizational influence

- Champion actively advocating internally

✅ Competition:

- All alternatives identified (competitors, incumbent, status quo)

- Competitive position understood

- Differentiation strategy defined

- Winning strategy against alternatives in place

Why MEDDPICC Practice Is Critical for Financial Services

Financial services MEDDPICC requires navigating regulatory terminology, understanding risk management priorities, and managing conservative multi-stakeholder qualification - skills that demand specialized practice.

What Makes Financial Services MEDDPICC Challenging

Regulatory Fluency: Understanding financial regulations, compliance requirements, and examination processes well enough to ask intelligent qualification questions.

Risk-Focused Mindset: Navigating conservative decision-making where risk mitigation is more important than potential benefits.

Stakeholder Complexity: Mapping and qualifying across compliance, risk, IT, legal, finance stakeholders with different priorities.

Long Conservative Cycles: Maintaining MEDDPICC discipline across 12-24 month sales cycles with multiple committee approvals.

The Financial Services Practice Problem

Colleagues Lack Regulatory Context: Traditional role-play doesn't include regulatory knowledge or financial services organizational dynamics needed for realistic qualification.

Missing Conservative Resistance: Generic practice can't replicate the risk-averse pushback typical in financial services.

No Regulatory Depth: Most practice scenarios lack the compliance complexity that drives financial services decisions.

How Sellible Masters Financial Services MEDDPICC

AI Prospects Who Understand Financial Services

Regulatory and Risk Fluency Sellible's AI understands financial regulations, speaks compliance language, and responds like actual risk officers, compliance managers, and conservative financial executives.

Multi-Stakeholder Scenarios Practice qualification conversations with AI representing different financial services stakeholders - compliance officers, risk managers, CFOs, IT security - each with different conservative priorities.

Financial Services-Specific Qualification Work through MEDDPICC qualification with AI prospects who discuss regulatory requirements, risk management, examination findings, and conservative approval processes.

Progressive Financial Services MEDDPICC Difficulty

Community Financial Institutions Practice with smaller banks and credit unions with simpler stakeholder structures but tight budgets and conservative cultures.

Regional Financial Services Work through more complex multi-stakeholder processes with regional banks, insurance companies, and investment firms.

Enterprise Financial Institutions Handle advanced scenarios with large banks, national insurance companies, or investment firms with extensive committee approval processes.

Implementation Plan for Financial Services MEDDPICC

Week 1: MEDDPICC and Regulatory Foundation

- Days 1-2: Learn MEDDPICC framework and financial services-specific application

- Days 3-5: Practice basic qualification with financial services-focused AI prospects

- Weekend: Review financial regulations and organizational structures

Week 2: Multi-Stakeholder Risk Qualification

- Days 1-3: Practice qualifying across compliance, risk, IT, and financial stakeholders

- Days 4-5: Work on identifying and developing champions in conservative organizations

Week 3: Complex Financial Services Deal Qualification

- Days 1-2: Practice complete MEDDPICC qualification on realistic financial services deals

- Days 3-5: Apply skills in real prospect calls while continuing practice

Ongoing MEDDPICC Mastery

- Daily Practice: 15-20 minutes focusing on regulatory qualification and conservative objection handling

- Deal Reviews: Use Sellible to practice upcoming qualification calls

- Regulatory Learning: Stay current with financial services regulations affecting buyer priorities

Conclusion

Financial services sales success requires disciplined qualification across regulatory, risk, technical, and financial dimensions. MEDDPICC provides the framework to qualify effectively in this conservative, risk-averse environment.

But executing MEDDPICC in financial services requires understanding regulatory requirements, risk management priorities, and conservative decision-making cultures. You must ask intelligent questions of compliance officers, risk managers, CFOs, and legal teams while managing long, committee-driven approval processes.

This expertise requires practice with realistic scenarios that include financial services stakeholder complexity, regulatory terminology, and risk-focused decision-making. Traditional role-play cannot provide this level of financial services-specific qualification practice.

Sellible provides the financial services-specific practice environment you need. Work with AI prospects who understand regulatory requirements, speak compliance language, and respond like actual financial services decision-makers across multiple conservative stakeholder roles.

Your competitors are running unqualified opportunities through long financial services sales cycles. When you master financial services MEDDPICC through realistic practice, you'll qualify effectively and focus on winnable deals in this challenging environment.

Ready to master MEDDPICC for financial services sales? Book a demo with the Sellible team and practice qualification conversations with AI prospects who understand regulatory complexity and speak financial services language.

Frequently Asked Questions

Q: How do I handle multiple conservative stakeholders in financial services MEDDPICC? A: Qualify each stakeholder separately focusing on their area (compliance, risk, IT). Map their risk concerns and relationship to economic buyer and approval committees.

Q: What if I can't access the economic buyer in a risk-averse organization? A: Work through your compliance or risk champion to understand economic buyer priorities. Request they arrange introduction framed around regulatory concerns.

Q: How long should financial services MEDDPICC qualification take? A: Initial qualification: 3-4 discovery calls across stakeholders. Complete MEDDPICC: 8-12 weeks across multiple conservative stakeholders and risk committees.

Q: What if stakeholders focus only on risk and ignore business benefits? A: Frame benefits in risk mitigation terms - regulatory compliance, operational risk reduction, examination preparedness. Connect ROI to risk management.

Q: How do I practice MEDDPICC with limited financial services regulatory knowledge? A: Start with basic financial regulations and risk management concepts. Use Sellible to practice with AI that provides regulatory context and conservative pushback.